The Lower Middle Market is Drowning in Capital

It's not your "daddy's market". Competition is everywhere. And the risk and return reflect that.

Fifty percent of direct loans to PE-backed sponsors now carry less than 500 basis points of spread. BB spreads in CLOs dropped 88 basis points year-over-year. And the lower middle market—once the last place in private credit where you could earn real yield—is being flooded by capital with nowhere else to go.

The conventional wisdom in private credit circles is that the LMM remains “underpenetrated.” That there’s still room to run. That the opportunity set is vast enough to absorb the wall of capital pointed at it.

The data says otherwise.

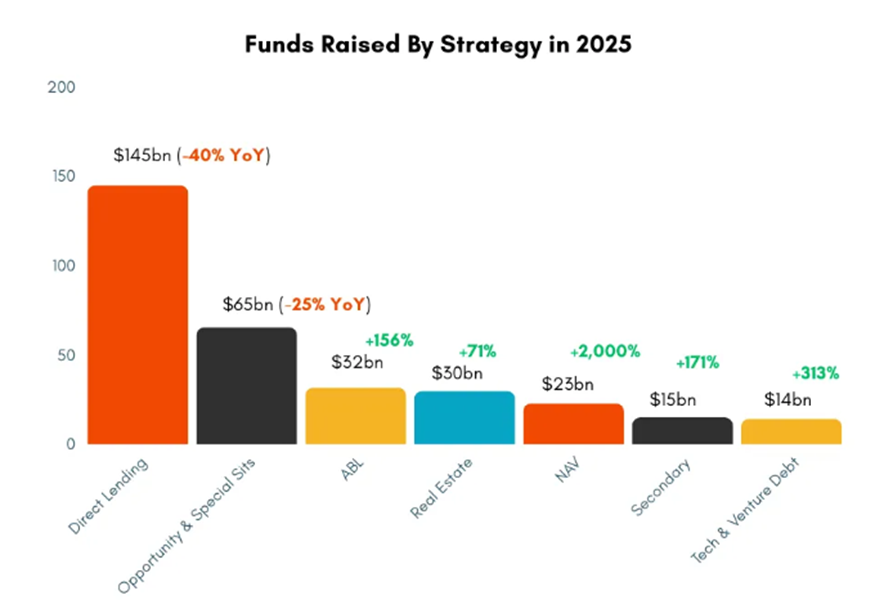

Let’s start with the main business driver for LMM credit players - equity sponsors. US middle market private equity is sitting on roughly $591 billion in dry powder. PE fundraising pace has been cut nearly in half year-over-year. Yet the capital already raised has nowhere to deploy—deal activity for direct lenders to PE-backed sponsors is down 24%, and new investments from the top 14 BDCs fell 11%. The machine raised the money. The machine cannot find the deals.On the credit side, the picture is equally swollen. Direct lending raised $145 billion in 2025, down 40% from the prior year but still the dominant strategy by a wide margin. NAV lending surged 2,000%. Venture debt up 313%. The smaller categories are exploding because the big ones are congested. Capital doesn’t disappear. It migrates. And right now, it’s migrating down-market in search of spread. (Pitchbook Q3 2025 Private Fundraising Report)

Source: “State of Private Credit in 2026”, Credit Crunch Substack.

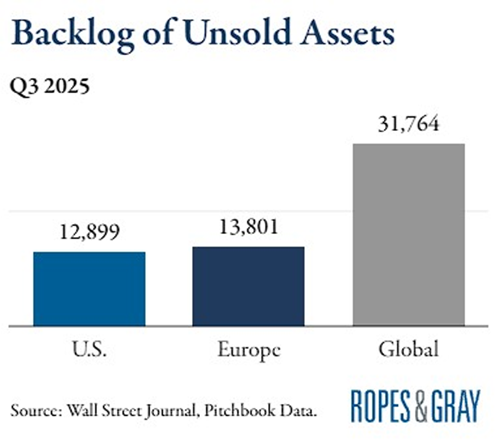

Meanwhile, nearly $1 trillion of dry powder remains untapped across all of US private equity. The backlog of unsold assets hit 12,899 in the US alone—31,764 globally—as hold periods lengthen and exits stall. This is not a temporary dislocation. This is structural congestion.

Source: Wall Street Journal, Pitchbook Data. Backlog of Unsold Assets, Q3 2025.

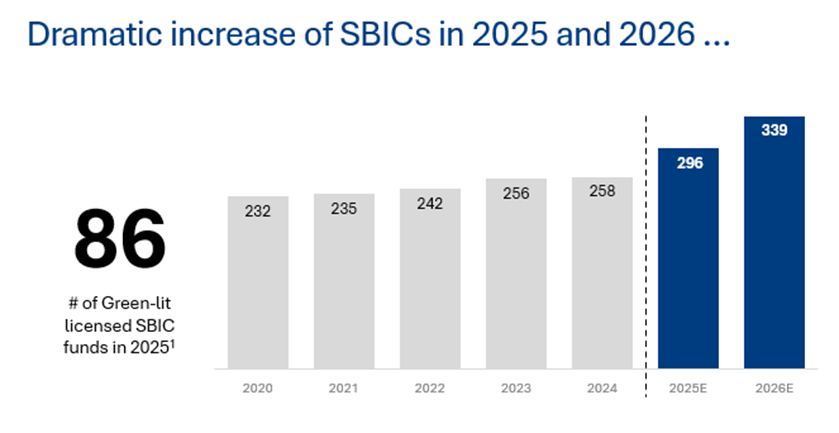

Now layer the SBIC program on top of this. The SBIC Program has been run by the Small Business Administration since 1958. It’s primary purpose is to “attract private capital to American Small Businesses”. The SBA guarantees debentures that allow SBICs to receive up to 2x leverage on their private capital to return mid-teen yields to LP for senior secured risk. (e.g., you raise $50mm from private institutions, SBA lends you $100 at ~10YT rates.)

The SBA green-lit (funds that SBA has approved but are in fundraising mode) a record 86 licensed SBIC funds in 2025. The pipeline suggests semi-annual debenture funds will grow from 258 in 2024 to an estimated 339 by 2026. On paper, this is the government accelerating capital formation into small businesses.

In practice, it’s fuel on a fire that’s already burning too hot.

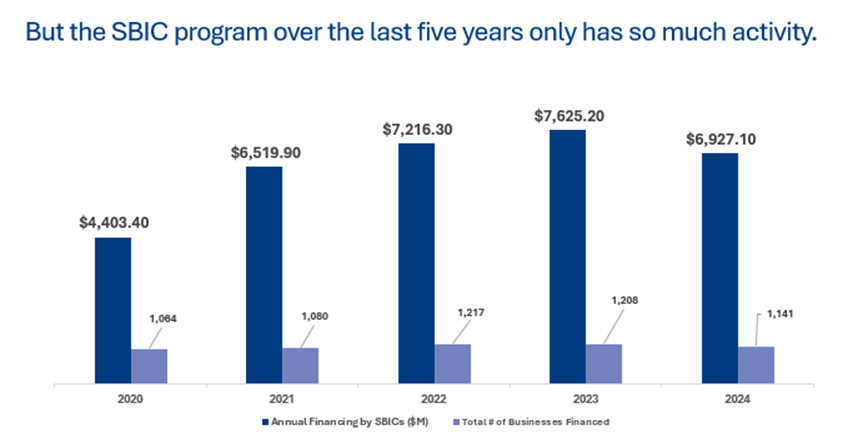

Here’s why. Annual SBIC financing peaked at $7.6 billion in 2023 and pulled back to $6.9 billion in 2024, covering roughly 1,141 businesses. Total SBA-reported assets in the program hit $54 billion by end of 2025. Against $29 billion in total SBIC financing over the last five years, that implies roughly $25 billion in unused SBIC dry powder at the start of 2026. That’s three times the average annual financing volume. And no single SBIC can invest more than 10% of its fund into any one deal. (SBA, SBIC Program Delivers Record Capital in FY 2025)

This causes even more congestion around the $3-$8mm EBITDA business realm. Too many funds chasing a finite set of lower middle market businesses, most with EBITDA under $5 million and inherent fragility baked into the business model.

Now put yourself in the seat of a direct lender trying to deploy capital in this environment.Of 1,200 Middle Market (EBITDA <$25mm) companies studied, 25% have debt coverage ratios below 1. Antares Capital’s CEO, Timothy Lyne, reported going from a “couple” debt-to-equity conversions a year to “more like eight or nine” in 2025. The credits are deteriorating, and the yields are compressing simultaneously. That’s not a market inefficiency you can arbitrage. That’s a market telling you the risk-return is broken. ( Marblegate Asset Management)

And the demand side is making it worse. The fundless sponsor model has become institutional in the LMM. Forty-four percent of independent sponsors reported receiving financing from SBICs in 2025. Seventy-nine percent are targeting $2–5 million EBITDA businesses. Independent sponsor LMM deal count posted a 51% four-year CAGR from 2019 to 2024. Searchfunder alone has over 3,000 active searchers, and the SBA 7(a) program supported more businesses in 2024 than at any point since 2008.

Source: Citrin Cooperman, McGuire Woods. Closed Deals by Buyer Type.

This is the mechanism by which dry powder becomes bad debt. Fundless equity partners pair with levered SBICs to acquire small, fragile businesses at rising multiples. Many independent sponsors are early-mid career former PE deal guys realizing that they’ll never see carry the way they dreamed, so they set out on their own to capture it. They’re professional, trained, and sharp. They are sophisticated and won’t get fleeced like some “mom and pop” baby-boomers retiring who don’t really know how much their business is worth

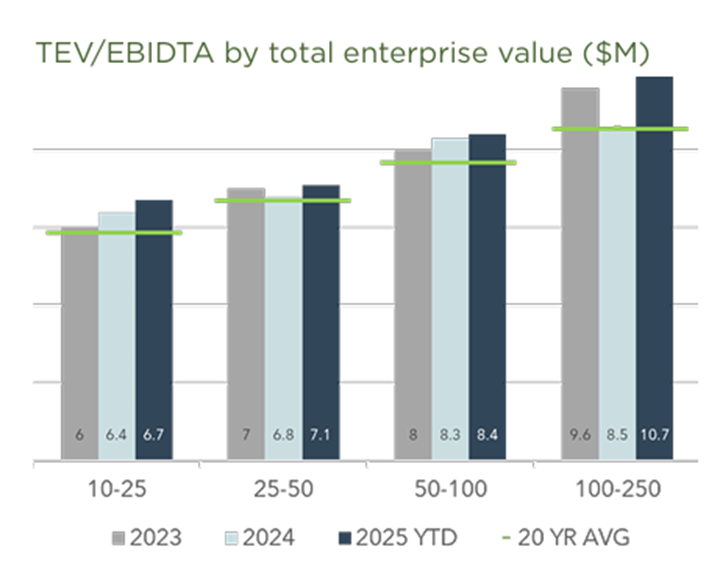

.GF Data’s Bob Dunn said it plainly: the competition for high-quality businesses is “at an all-time high.” Assets that used to trade at 4–6x EBITDA now change hands at 6–9x. A business generating $9 million in EBITDA is fetching a $100 million purchase price.Let that sit for a moment. A $9 million EBITDA business. $100 million price tag. In the lower middle market. (I've seen $2.5mm EBITDA businesses fetch 8x - makes me wonder why I decided to become an investor and not a business owner.)

But this is where the businesses are traditionally more fragile, have higher customer concentration, require manual-technical skills (e.g., MRO, HVAC, etc.) the management teams are thin, and the margin for error is nearly nonexistent. Which is why yields were traditionally higher and attractive for LPs.

We have private credit funds, SBICS, and a push back from the OG credit providers:

The banks.

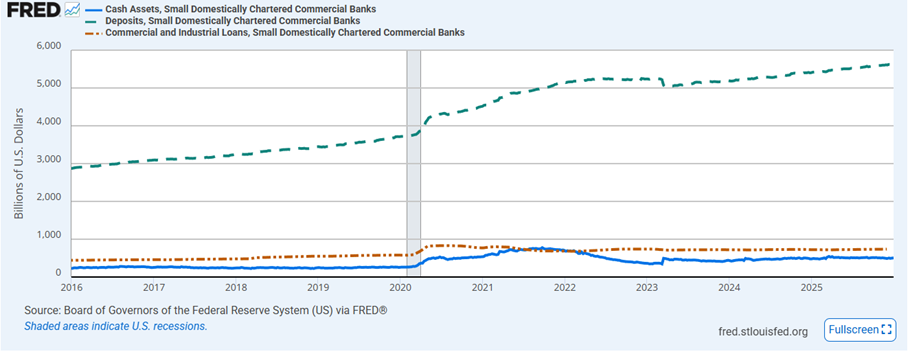

And to their credit, regional banks are recovering from the 2023 liquidity crisis and re-entering direct lending—but selectively.Cash assets remain stable. C&I loans hold steady in absolute terms. But C&I as a proportion of deposits has dropped 220 basis points since 2016. The big banks are scaling lending aggressively; the regionals are cherry-picking the safest credits and leaving the riskier paper to private lenders.

(FRED; PwC, Lending’s Next Act)

This creates a bifurcation that should concern every allocator in the space. At the top of the market, banks compete on cost of funds and win. In the lower middle market, private credit funds absorb the risk the banks won’t touch—and with heavy competition, driving down yields. Or forcing credit players to compete on equity injections, looser docs, and speed.The credit landscape by deal size tells the story clearly.

Below $5 million in debt ticket need (or up to $10mm for manufacturing acquisitions), borrowers rely on SBA 7(a) loans with personal guarantees, placed by banks at SOFR +350–400—roughly 8.25% at Huntington Bank—on 10-year amortization. The $5–10 million band is a credit gap: investor brain damage from prior cycles, inherent business fragility, and regional bank disinterest make it a no-man’s-land.

The $10–20 million range is prime territory for SBICs and regional banks, but it’s heavily reliant on M&A volume that isn’t materializing. And now heavily on independent sponsors who will throw the keys to a credit investor and have to rely on others to solve problems on the equity side. (Imagine a business taking a bad break and then having to raise external capital, CEO is bailing water out of a sinking ship while trying to convince other passengers to step onboard.)

And above $35 million, you’re in mid-market territory, facing downward pressure from larger credit funds desperate to deploy.Every segment is congested. Every segment is competitive. And in every segment, the incentives are pushing participants to take risks they shouldn’t

.A bad storm is brewing. And like most storms in finance, it won’t arrive as a single dramatic event. It will be a slow accumulation of bad decisions made under the pressure to deploy capital.

The thesis is straightforward. Too much equity capital chasing too few deals drives down quality and drives up multiples. Too much debt capital chasing those same deals compresses yields, loosens documentation, and pushes loan-to-value ratios higher. The fund managers who can’t deploy face existential pressure—this may be the last fund they can raise, so they need to take risks.The LPs who gave them capital hear, “We’re not paid to hold cash. If you want risk-free, buy treasuries.”

(And if you’ve heard that line from a GP recently, you should be concerned about what comes next.)

The likely winners on the equity side are niche operators with genuine scale advantages—firms that can actually improve business operations, develop moats, and create value beyond financial engineering.

On the debt side, the winners are those with the lowest cost of funds and religious underwriting standards, those with the courage to pass.

Everyone else is heading toward “pray and delay” mode—a mindset driven by deal velocity incentives and the comforting belief that “we’ll work it out.”

The counterarguments are real.

A 10-year yield drop could ease pressure. Continuation vehicles and PE secondaries provide liquidity. The rise of ABF funds, NAV lending, and specialty finance could unclog exits. A resurgent IPO market could change the math entirely. Maybe AI solves enough operational inefficiency to justify these multiples. Or maybe very talented former VPs from Blackstone and KKR can create real value across the middle market.

Maybe. But these are mechanisms for the core and upper middle market. They don’t solve the fundamental problem in the LMM: too many undifferentiated funds chasing fragile businesses with capital they’re incentivized to deploy regardless of quality.

The private equity and lending markets are as saturated and competitive as public markets—yet face more perverse incentives.

In a public market, the price moves in real time and you can exit in seconds. In the lower middle market, you’re locked in for years with a business that might not survive the next tariff shock, the next rate move, or the founder’s decision to retire – all during a volatile geopolitical environment unrivaled since 1989 or maybe even 1939. And potentially the most disruptive human technology since the nuclear bomb or fire.

The punchline?

This isn’t our “daddy’s market”.

There is no free lunch in private investing either.

Comments ()